VENTURE FUNDING TRENDS

Funding dips amid a volatile macro environment

Fewer mega (>$500M) robotics and AI-related rounds have contributed to overall reduced investment volume in 2025, with quarterly funding at or below the 2021-2024 average. This is exacerbated by a challenging year for climate tech legislation, with the rollback of a number of key incentive policies across the US and Europe. That said, reporting delays and the likely announcement of a handful of mega rounds in Q4 could see the annual funding gap narrow over the coming months, mirroring what was seen in 2024.

US startups continue to attract more capital across the board, but Europe remains an electrification hub

While the US leads in both early and later stage dollars invested, 2025 deal volume is evenly distributed across key climate investment themes, including grid technologies, building efficiency and building electrification. Notably, funding for AI robotics applications in the built world - such as asset digitisation, manufacturing automation, asset and construction operations, and risk management (driven by disaster response and weather models) - remain highly concentrated in the US market.

US on track to claim >60% of the market in 2025, with the UK set to shrink by >60%

Built world funding resilience in the US and mainland Europe contrasts with rapidly declining investment in the UK. This is consistent with an overall slowdown in the UK venture landscape outside of built world themes, with Q22025 reported by KPMG as the slowest since early 2020.

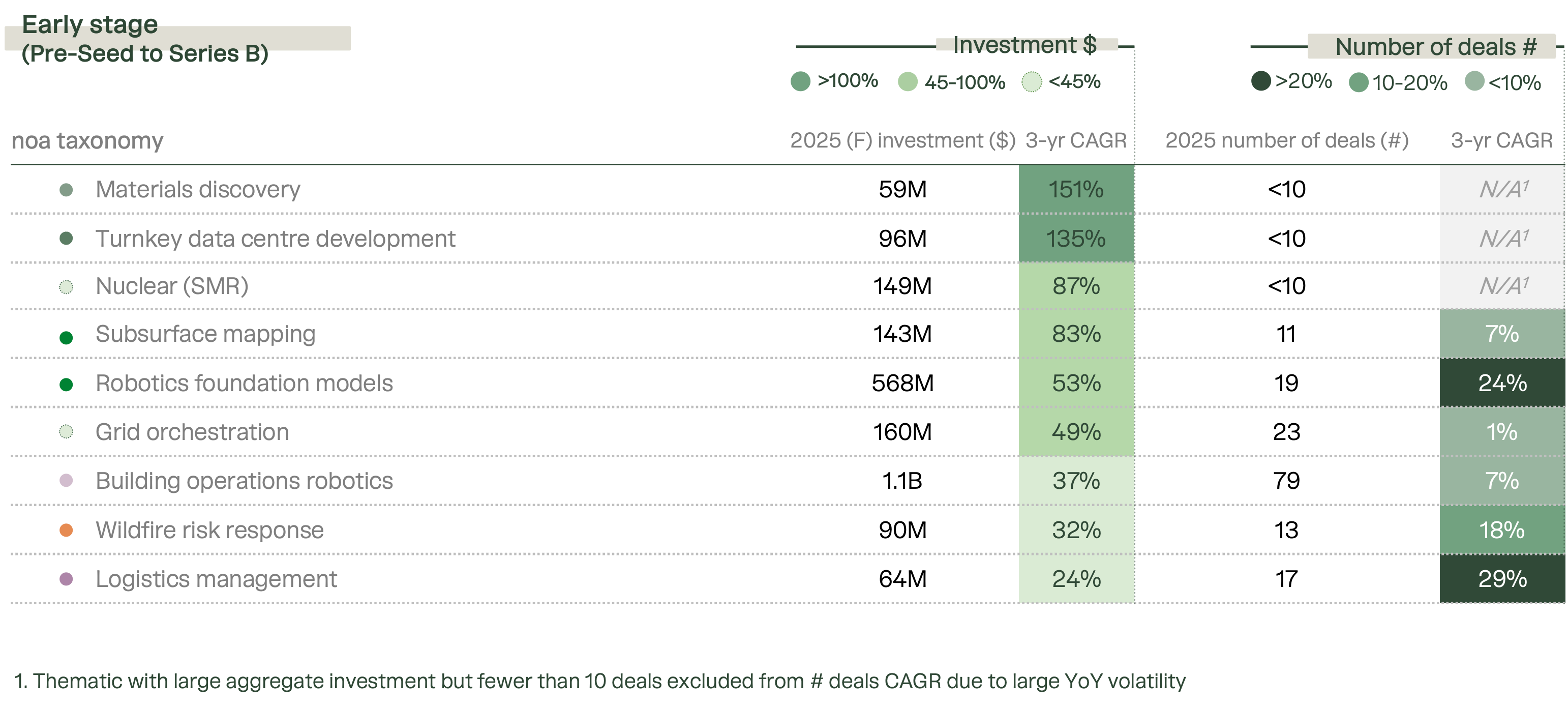

Built world tech’s fastest growing investment themes sit at the intersection of artificial intelligence, energy and industry

Digging deeper into the specific investment subcategories, it’s clear that rapid innovation is unlocking new capabilities across materials discovery, robotics, manufacturing, network optimisation, and advanced analytics. Simultaneously, frontier AI labs are increasingly deploying capital to address bottlenecks caused by the limitations of data centre and power generation capacity.